Finance Team

Cash Management

Sponsors can choose one of three methods to remit payment to Washington State University for settlement of reimbursement on awards. Sponsors can make payments by check, Automated Clearing House (ACH) or Wire. It is important that payment includes a reference to the award or project, which may include:

- Invoice number

- Award Number

- ORSO Number

- Principal investigator name

- Project title

Please include in the message field what the payment is for, such as the invoice number, award number, project title, Principal Investigator’s name, and/or ORSO number.

- All requests for banking information should be sent to the Sponsored Programs Services Mailbox (sps@wsu.edu).

- The SPS Finance team will complete all relevant banking fields on the request form for ACH and Wire payments.

All sponsored check payments should be sent directly to Sponsored Program Services using the address below.

Washington State University

Office of the Controller

Sponsored Program Services

240 French Administration Building

PO Box 641025

Pullman, WA 99164-1025

Option to deliver checks in person to the front desk of the Controller’s Office. (Address Below)

Sponsored Programs Services

242 French Administration Building

Pullman, WA 99164

Checks and any remittance advice or backup received with a check in a department or WSU Extension location for payment on sponsored projects must be forwarded to SPS for processing.

We discourage sending checks via university interoffice mail since it is difficult to track these deliveries.

Invoicing

Contact SPS@wsu.edu for information regarding invoices or invoicing.

Depending on the payment terms of an award, SPS Finance may be required to submit an invoice to initiate payment by the sponsor. At award set-up, SPS Finance determines the deliverable type and records the invoice period and due dates of each invoice. There are two general categories of invoices as well as an advance or “upfront” payment type:

- Cost Reimbursable – an invoice that itemizes project expenditures that have been incurred and requested for reimbursement by the sponsor. These payment requests are generally invoiced monthly (frequency varies by sponsor).

- Fixed Price – an invoice for a fixed amount that is predetermined based on the payment schedule of an award and in some cases requires the completion of project deliverables or milestones to coincide with the invoice submission

- Advance Payments – An “upfront” payment or schedule of payments that occur before the start of a project or ahead of expenditures on the general ledger. Some advance payments require the submission of an invoice.

When requested, the department/local level managing unit provides a validation of programmatic and/or financial information prior to SPS Finance submitting an invoice to the sponsor. Throughout this process, the status of each invoice is tracked in Workday. Once an invoice is submitted to the sponsor, SPS Finance records the receivable in Workday.

Letter of Credit

Most federal sponsors authorize Letter of Credit (LOC) as the cash mechanism for providing cash disbursements to award recipients. For Federal sponsored awards, payment is requested and received on a cost reimbursement basis via a LOC. SPS Finance is responsible for preparing and performing the LOC draws across federal agencies that utilize a LOC. SPS Finance processes these drawdowns through each sponsor’s respective online LOC system.

Most of the federal agencies allow grantees to draw the funds up to 90 days after the award expiration date. NIH and NSF allow for an additional 30 days to draw funds, allowing for a total of 120 days after the award expires. Any LOC draw requests that exceeds the draw deadlines of 90/120 days will be rejected by the sponsor. In addition, the federal sponsors require the total LOC draw amounts for each award to match the total expenditures reported on the final Federal Financial Report (FFR), which is filed using the SF-425 financial report.

SPS Finance works closely with the department grant managers to ensure the LOC funds are fully drawn to offset the award expenditures within the 90/120 day draw deadlines. As part of this process award expenditures reported on the final FFR are reconciled to the amount drawn for the expired award. SPS Finance also draws on a biweekly basis to align with payroll.

Accounts Receivable

The Finance Team utilizes the Workday system to:

- Invoice external sponsors for sponsored project awards

- Apply payments to invoices

- Place “on-account” funds received by sponsors which cannot be immediately applied to a specific invoice

- Track and report on receivable items, activity, and payments

SPS Finance provides monitoring and oversight of outstanding accounts receivable and performs ongoing collections of any payments that are more than 120 days overdue. Collection efforts are initiated by the SPS Cash Management team. In some instances, Cash Management may require the assistance of the departmental grants administrator in collecting outstanding receivables.

Recovery

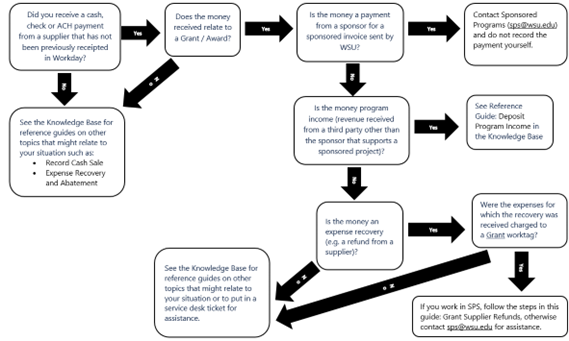

Grant Supplier Refunds (Expenses Recoveries on Grants)

An expense recovery refers to a situation where an expense has been charged, but the amount later needs to be reduced, such as in cases where goods are purchased for use on a grant, but the supplier has overcharged and sends a refund back to WSU. Payments received from sponsors for reimbursement of grant expenses, and program income revenue are not expense recoveries and have their own processes for recording the funds received.

Before you begin, review the decision tree below to determine whether the Recovery process applies to your situation.

Program Income

Workday Grants Guide: Deposit Program Income

Departments who receive program income should record program income funds using the Record Cash Sale task in the Workday system. Once the program income is recorded correctly, SPS Finance will be notified, and the program income transferred onto the appropriate award. This reference guide provides information on how to record and deposit a cash sale.

Program Income is the income earned by an awardee that is directly generated by a sponsored activity or earned because of a sponsored activity. Program income must be identified, appropriately documented, and the resulting revenue and expenses properly recorded and accounted for. Both federal and non-federal sponsored awards generally require similar diligence to identify, document, and account for program income. As a result, program income on federal and non-federal sponsored awards is subject to this guidance. However, if a non-federal sponsor, or a firm-fixed price sponsored award, is silent on the issue of program income, the income is not reportable and therefore not considered program income.

Examples of program income include the following when the source of funding is a sponsored award or the revenue is directly generated by a sponsored activity (note that royalties from patents, copyrights, etc. are generally not reportable as program income):

- Fees earned from services performed under the project, such as laboratory tests

- Income generated from sales of commodities and research materials, such as tissue cultures, cell lines, and research animals

- Registration fees from participants attending conference or workshop

- Income from sales of educational materials

- Sale, rental, or usage fees, such as fees charged for the use of computing or laboratory equipment

- Income generated from the sale of software, digital media, or publications